Week In Review

Thank you for being part of our Week in Review newsletter. While this will be our last Week in Review, we are excited to continue bringing you financial market updates through our merger with Nicolet National Bank.

The Vault Blog brings you monthly newsletters and quarterly outlooks from the investment team at Nicolet Wealth Management, keeping you up to date with the latest action in financial markets. Head to nicoletbank.com/blog for the more insights.

02.13.26

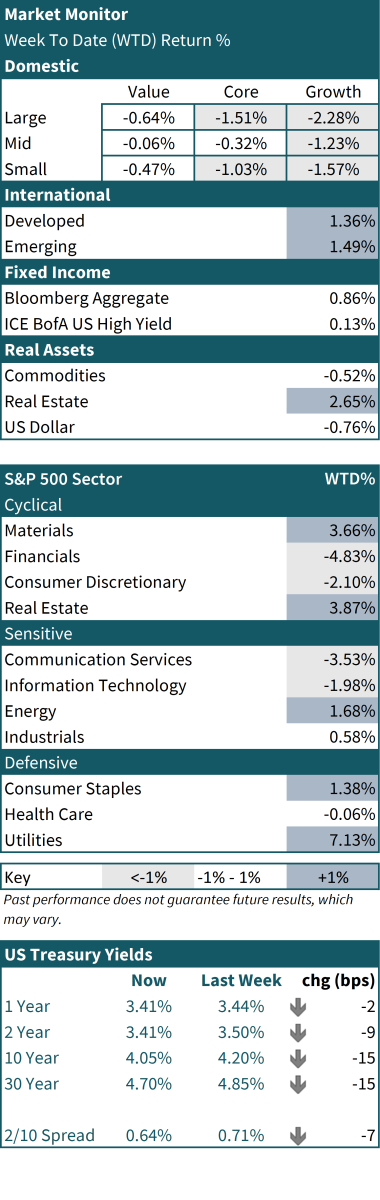

- U.S. equities mostly lower; Small Caps and Value held up better than Large Caps and Growth.

- Defensives led: Utilities, Materials, and Real Estate outperformed; Financials and Communication Services lagged.

- Overseas markets continue to lead, with Developed outperforming Emerging.

- Rates drifted lower in response to economic data and bouts of “risk-off” sentiment; volatility rose as the dollar softened.

- Inflation data continues to be well-behaved; labor indicators pointed to stabilization; December retail sales softened.

- Policy backdrop remained fluid: tariff‑relief chatter resurfaced and deficit projections widened.

U.S. stocks posted modest weekly declines, with the major large‑cap indexes down and Small Caps faring comparatively better. International benchmarks outperformed, and commodities were lower on the week. Volatility rose while the U.S. dollar weakened.

Leadership continued to rotate away from mega‑cap growth toward defensives and rate‑sensitive sectors. Value topped Growth and Small Caps outperformed Large Caps. Utilities, Materials, and Real Estate led among sectors, while Financials and Communication Services lagged. Overseas, Developed Markets—led by Japan—outpaced Emerging Markets, where China remained a drag. Tone throughout the week leaned cautious rather than risk‑off on the whole, with volatility higher, the USD lower, and oil weaker.

AI remained a headline fixture, but the signals were mixed and stock‑specific. Big‑tech underperformance revived questions about the ROI of large AI capex and buyback capacity, and remarks from Microsoft’s AI leadership about rapid automation of white‑collar tasks sharpened disruption risk. The “disruption trade” widened beyond software as insurance brokers, financial advisors, commercial real estate brokers, and freight brokers sold off on product headlines from Insurify (insurance tools), Altruist (tax‑planning chatbot), and Algorhythm Holdings (AI‑enabled freight scaling). Offsetting that, operators and investors emphasized software’s durability and enablement benefits—Amazon AWS highlighted SaaS leverage to AI, while Apollo, Vista, and Thoma Bravo pointed to healthy portfolio fundamentals. Adoption datapoints improved (OpenAI noted ChatGPT back to >10% m/m growth), TSMC posted stronger‑than‑expected +37% y/y January sales, and several AI‑infrastructure beneficiaries showed post‑earnings strength, including Vertiv, Generac, Arista Networks, Credo Technology, and Applied Materials.

Inflation updates supported a “steady disinflation” narrative. Headline CPI increased 0.2% vs the prior month and the year-over-year change was 2.4%, the lowest in eight months. January core CPI rose 0.3% month-over-month, in line with expectations, while the year-over-year reading printed at 2.5%, the lowest since March 2021. Core goods were flat while core services accelerated to 0.4%; shelter rose 0.2% and remained the largest contributor to the monthly increase. Disinflation was most evident in energy and used autos, while airfare and apparel posted gains. Treasury yields fell, led by the long end, a move consistent with favorable inflation, and periodic bouts of “risk-off” sentiment from AI concerns throughout the week.

Consumer signals were mixed into year‑end, and earnings were broadly constructive. A New York Fed read showed 4.8% of outstanding debt in some stage of delinquency in Q4, and counseling data pointed to rising financial strain among higher‑income cohorts than before the pandemic. December retail sales were flat versus expectations, with the control group down modestly and weakness broad across home‑related, apparel, and electronics; a few bellwethers offered more constructive updates. With ~74% of S&P 500 companies reported, blended Q4 EPS growth stands near 13%, up from ~8% at quarter‑end; blended revenue growth is ~9%. Beat rates are mixed—about 74% have topped EPS (below recent averages) and ~73% have topped sales (above recent averages)—with aggregate EPS surprises near +7% and revenue surprises around +1½%.

January nonfarm payrolls rose by 130K, the unemployment rate ticked down to 4.3%, average hourly earnings increased 0.4% m/m, and average weekly hours improved to 34.3. The annual benchmark revision subtracted about 862K jobs from the 12 months through March, effectively lowering last year’s average monthly pace; the revision was an improvement from the September estimate which anticipated a revison of -911k jobs. Methodological changes also mattered: one desk estimated that adjustments to net business formation added roughly 70K to January versus December, suggesting the headline may somewhat overstate underlying momentum.

Policy and credit themes stayed in focus. Deficit projections for 2026–2035 moved higher versus prior estimates, keeping fiscal dynamics in the conversation. Reports suggested potential scaling back of some steel and aluminum tariffs, and a symbolic House vote added to expectations for tariff relief ahead of the midterms. From a micro vantage point, takeaways from a major financials conference were constructive: management tone improved on fading tariff headwinds and fiscal tailwinds, C&I lending showed momentum through January, and sentiment on M&A and capital markets remained upbeat. Positioning indicators also looked cleaner, with retail sentiment moderating and software exposure notably light.

Key events to watch next week

Consensus estimates in parentheses unless otherwise noted.

Monday: Markets are closed for Presidents Day

Tuesday: The Empire State survey and the NAHB index—early reads on factory activity and builder sentiment

Wednesday: Building Permits, Housing Starts, and Durable Goods, adding color on residential supply and capex intentions

Thursday: Jobless claims, Existing Home Sales, the Philadelphia Fed index, and Pending Home Sales offer timely checks on labor turnover and housing demand

Friday: The first estimate of GDP, the PCE Deflator (the Fed’s preferred inflation gauge), Personal Income, S&P Global PMIs, and New Home Sales. Earnings continue, with updates from Walmart, Deere, Toll Brothers, Analog Devices, and Booking Holdings—likely to be useful read throughs on the consumer, industrial demand, housing, semis, and travel.

Past performance does not guarantee future results, which may vary.

Source: FactSet, MidWestOne Private Wealth.

All returns presented are total returns, which include the reinvestment of income and dividends.

For style performance, Large, Mid, and Small for US Equity refer to the Russell 1000, Russell Midcap, and Russell 2000 indices, respectively. Value refers to companies with lower price-to-book ratios and lower expected growth values, and Growth refers to higher price-to-book ratios and higher forecasted growth values. Real Estate refers to the DJ Equity REIT Total Return Index. Commodities refer to the Bloomberg Commodity Index. US Dollar refers to the value of the United States dollar relative to a broad basket of trade-weighted foreign currencies. Developed: MSCI EAFE; Morgan Stanley Capital International Index that is designed to measure the performance of the developed stock markets of Europe, Australasia, and the Far East. Emerging: MSCI Emerging Markets; Morgan Stanley Capital International Index designed to measure the performance of the emerging stock index of China, Brazil, India, and other emerging market countries.

Diversification does not protect an investor from market risk and does not ensure profit.

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. Views and opinions expressed are current as of the date of this publication and may be subject to change, they should not be construed as investment advice.

John McClain

Kong Her

Bill Neal

Tell us about you.

Realize your vision for the future through careful planning, expert guidance and a disciplined, collaborative approach that grows with you and your passions.

Not FDIC Insured | No Bank Guarantee | May Lose Value | Not a Deposit | Not Insured by any Federal Government Agency